MSE435 · Lecture 01: Intro: The AI Supercycle.

Lecture notes on where value accrues in the AI value chain, why the triangle is inverted today, and how long it takes to flip — from Apoorv Agrawal's intro to MSE435 at Stanford.

MSE435 · Lecture 01: Intro: The AI Supercycle

Lecture notes. Apoorv Agrawal · Altimeter Capital · Stanford MSE435.

The question the course reduces to

Where's the money? Where's the money in AI? Apoorv Agrawal, opening the class [00:00:27]

Why this course

Apoorv's one-line reason for teaching it: "this is such a big super cycle" [00:04:09]. The course walks the AI value chain one layer at a time — chips, infra, models, apps — with a guest operator from each layer.

Why take this course — the tech-wave frame

Each wave seeded a new generation of category-defining companies. GenAI is the next one, and it's only three years in.

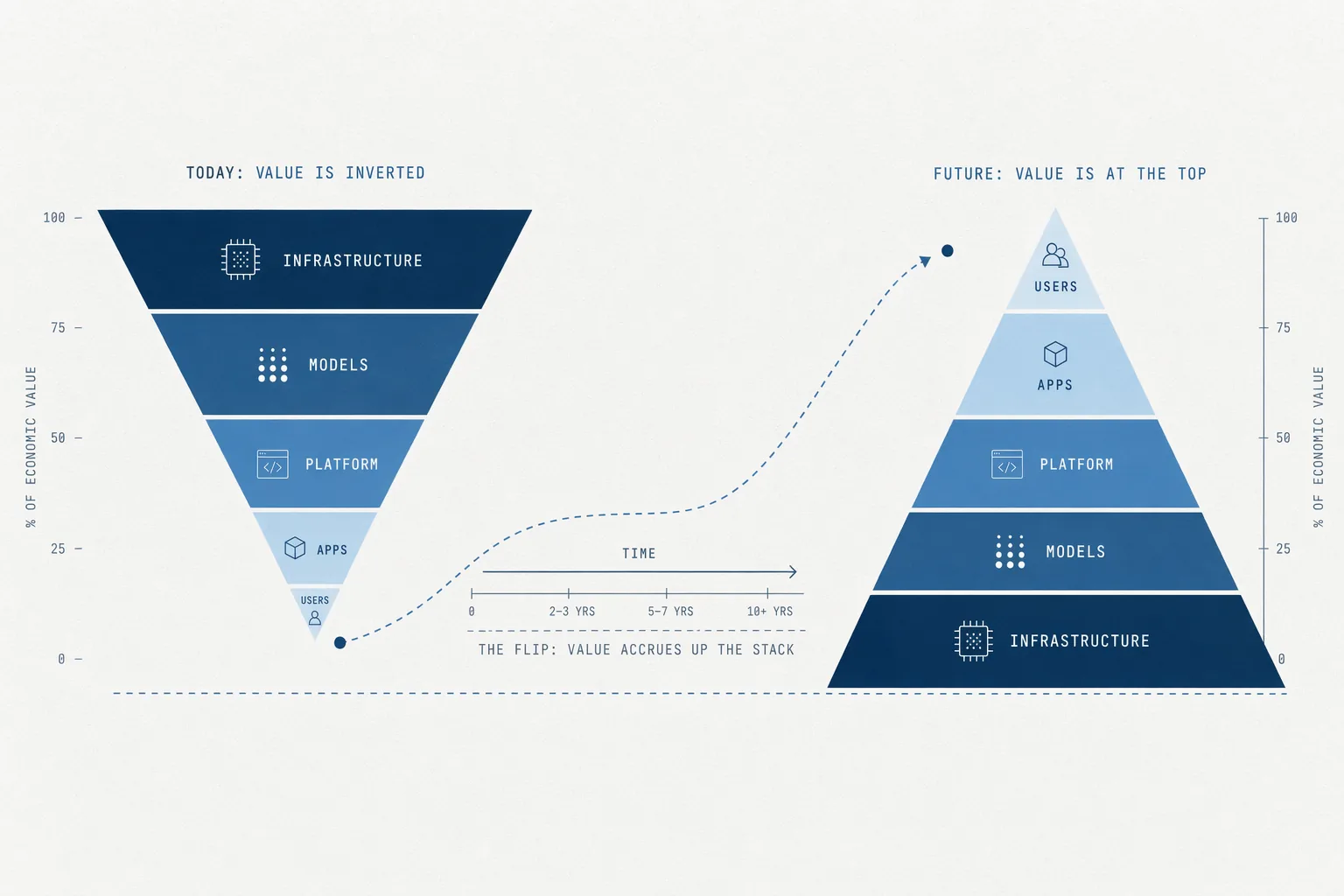

The thesis: the triangle is inverted

Every prior super-cycle (internet, mobile, cloud) eventually had more revenue at the apps layer than at the infra or chips layer — a pyramid with a wide top. AI today is the opposite: narrow at the top, wide at the base [00:07:20].

Software ate the world because, you know, I could distribute it to millions of people and the marginal cost of running that software was close to zero. … The incremental user of an AI application is not free. It's actually quite a bit more expensive to have AI users because turns out you've got to burn those GPUs. Apoorv Agrawal [00:08:20]

Where does value accrue in AI?

Estimated annual revenue per layer. Cloud matured apps-heavy; AI today is the mirror — chips-heavy. The question is how long before AI inverts too.

Cloud's playbook: eight years from breaking ground

If AI's triangle is going to flip, how long does that take? Apoorv's reference point is AWS.

AWS started in the year 2004. AWS has its first customer in Netflix in 2010. And ultimately, Amazon shifted fully to AWS in 2012 — eight years from breaking ground. Apoorv Agrawal [00:09:54]

The AI substrate — GPUs, interconnects, memory, energy — is harder to commoditize than virtualized x86 was, so Apoorv's working bet is that this one takes longer than cloud did.

AWS revenue, 2004–2026 — the three phases

- 2004–2009 · seeding. AWS invisible as a revenue line; Amazon itself wasn't yet on it.

- 2010–2012 · Amazon migration. Netflix became first real customer in 2010; parent company fully on AWS by 2012.

- 2013–2026 · mainstream. Apps layer catches up, AWS compounds into a ~$140B run-rate.

Where profit concentrates today

The most profitable part of the stack is the semis layer, by a long shot. Apoorv Agrawal [00:19:58]

The revenue share is as lopsided as the profit share: roughly ~75% of the ~$350B of new AI revenue added over the past 24 months landed at the chips layer. And margin persistence there is still increasing, not dissolving [00:20:00].

Chips capture ~75% of new AI revenue, last 24 months

Of the ~$350B of new AI revenue added to the ecosystem between Apr 2024 and Apr 2026, roughly three out of every four dollars ended up at the chips layer.

Consumer AI apps are going mainstream

Apoorv benchmarks AI-app adoption against the non-AI consumer leaders — using weekly active users (WAU, unique users who open the app at least once in a 7-day window) as the yardstick. The comparison is stark: ChatGPT is ~800M WAU and climbing, Gemini is the only other meaningful line, everything else hugs the x-axis [00:34:00].

Consumer apps — weekly active users

Three natural tiers. Core utility (YouTube, Chrome, WhatsApp) at ~3B WAU. Social (Facebook, Instagram, TikTok) at 1–1.5B. Niche (Spotify, Amazon, X) at ~400M.

AI apps — weekly active users

ChatGPT is an outlier at ~800M WAU. Gemini has broken out to second place at ~220M. The long tail — Claude, DeepSeek, Character AI, Perplexity, Grok — each sit under 50M.

Apoorv's monetization baseline for the comparison: Alphabet runs ~4B users at ~$100/year ARPU (average revenue per user); Meta runs ~3.5B users at ~$70/year ARPU; ChatGPT is ~1B users at ~$10/year ARPU [00:37:43]. The unlock he expects is ads, on precedent from Facebook's mobile transition a decade ago.

Consumer & AI apps on the same axis

ChatGPT is climbing into the social-network band; the next step is reaching the core-utility band.