The Importance of Going Fast.

Speed gets talked about as a cultural value — "we move fast," "bias for action" — when it's actually a mathematical one. Going faster changes two variables that dominate long-run enterprise value: when you cross break-even, and what multiple the market pays you at exit. Bot

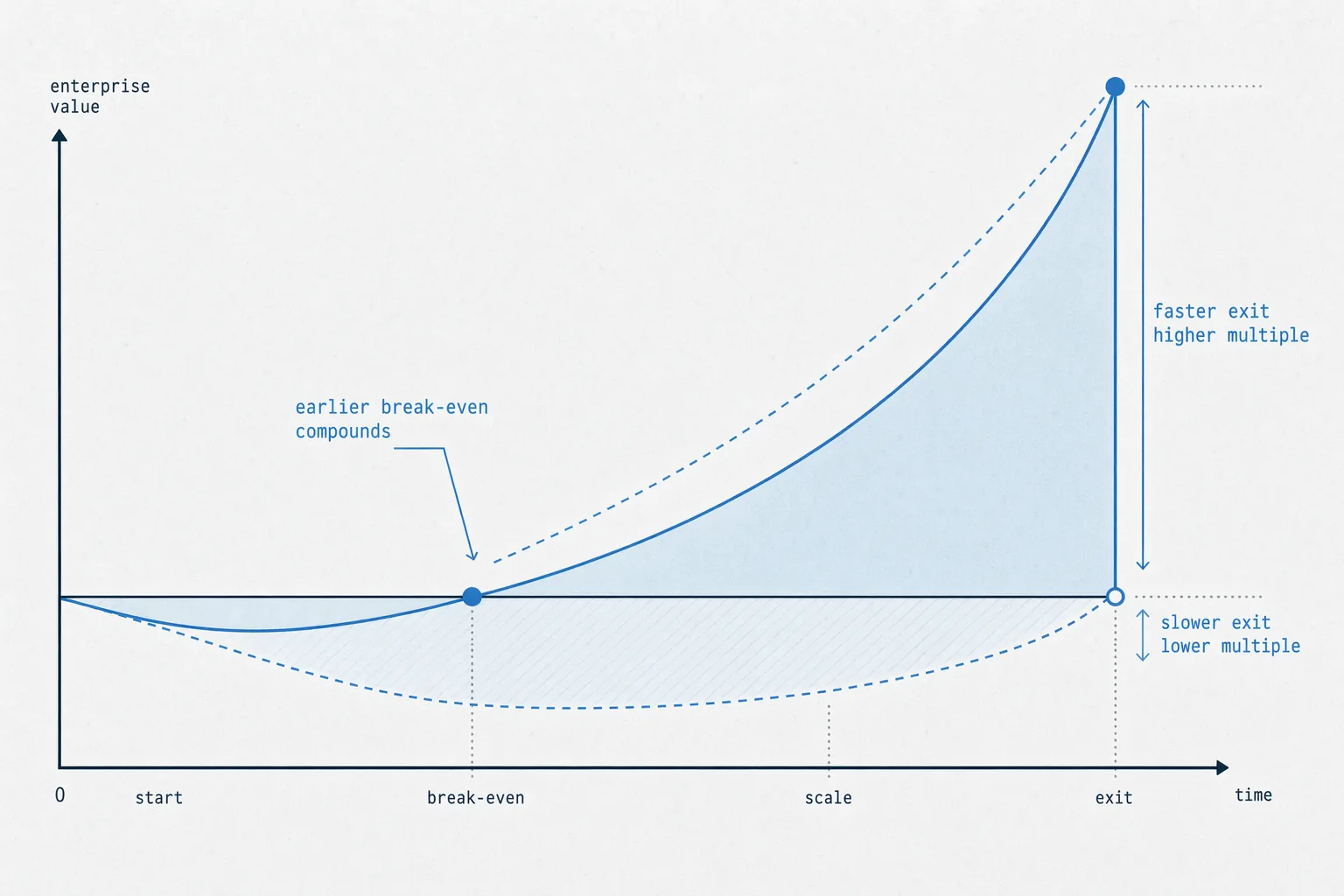

Speed gets talked about as a cultural value — "we move fast," "bias for action" — when it's actually a mathematical one. Going faster changes two variables that dominate long-run enterprise value: when you cross break-even, and what multiple the market pays you at exit. Both compound. Neither is recovered by working harder once they've slipped.

The break-even curve

Any operational change — a new location, a new product line, a reorganization — has the same profile. You consume value first (investment, ramp, cost) and produce value later (revenue, margin, productivity). The shape of that curve is what matters. Two companies making the same change can produce wildly different outcomes depending on how impatient they are about executing it.

Pull the break-even point forward by a single month and three things happen, not one:

- The value-consumed region shrinks — less cash burned before the change turns positive

- The value-produced region extends — more time compounding on the productive side of the curve

- The net contribution between the two is disproportionately larger than the one-month shift would suggest, because value-produced and value-consumed are integrating over time in opposite directions

A one-month acceleration is not a one-month improvement. The gain is the area between two curves over time — a trapezoid — and that area captures most of the value created.

The growth multiple effect

The second layer is what Credit Suisse's Corporate Insights group documented years ago in the Incremental Growth Curve: the multiple the market pays on your EBITDA is a non-linear function of growth relative to sector median. Moving from "below sector" to "moderately higher than sector" adds meaningfully more EV/EBITDA than the same step higher up the curve. This effect is strongest for asset-light, high-return-on-capital businesses (software, platforms) and weaker for capital-intensive or commodity industries. The effect is strongest for high-return-on-capital companies — the ones whose growth is most valuable — and nearly absent for low-return-on-capital ones.

Translation: if your returns on capital are good, the market will reward growth with a disproportionate multiple expansion. Going faster doesn't just produce more EBITDA, it produces EBITDA that is worth more per dollar at exit. Speed × growth-adjusted multiple is the real compounding equation.

A synthetic example

Imagine two identical operators launching the same new business line.

| Item | Fast operator | Slow operator |

|---|---|---|

| Time to break-even | 6 months | 12 months |

| Year-2 EBITDA | $8M | $6M |

| Exit multiple | 11.0× | 9.5× |

| Implied enterprise value | $88M | $57M |

This is the frame I keep coming back to when people talk about cost with no reference to foregone value. The famous Elon/SpaceX version:

Everything we did was a function of our burn rate. We were burning through $100,000 per day. In the same way I expected the revenue in 10 years to be $10 million a day, every day we were slower to achieve our goals was a day of missing out on that revenue.

Elon Musk on early SpaceX — via Founders Podcast #399, “How Elon Works” (David Senra, Aug 2025)

Delay is an opportunity cost measured against the future cash-generation rate, not just against today's expense line.

The operator's calibration

The test I try to run on any operational change:

- If we pulled break-even forward by 30 days, what would the incremental NPV be? If that's larger than the cost of moving faster, speed is underpriced. If the answer is bigger than the marginal cost of pushing harder, the slower plan is the wrong plan.

- What are we actually waiting for? Name it. If the answer is "alignment" or "readiness," push back — those are words that describe the absence of a specific blocker.

- What's the smallest increment we could ship this week? If the answer is "nothing, we need three more months of prep," the project probably isn't real yet.

The operators I've seen compound the most wealth have been unreasonable about this. Not reckless — reckless is a different failure mode — but consistently impatient with themselves and with their organizations.

The combined picture

The slide this post is built around shows both effects side by side for a reason. They're the same insight at two scales.

- At the operational scale, speed shrinks the value-consumed trapezoid and extends the value-produced one.

- At the enterprise scale, higher growth earns a higher multiple on a steeper part of a non-linear curve.

Growth helps everyone. Speed is what turns growth into growth that compounds. The companies that are worth the most at exit are not the ones that made fewer mistakes — they're the ones that made their mistakes earlier, fixed them faster, and spent more years on the productive side of the break-even line.

Source: Credit Suisse Corporate Insights, Incremental Growth Curve, Exhibit 5.